Ask any scenario. Know every risk.

Instant guideline answers and a live pipeline brief. Built for the loan officer who closes deals.

Purpose-built for mortgage.

Not a general chatbot.

Every agency rule. Cited by source.

Fannie Mae, Freddie Mac, FHA, VA, and USDA through 2026. Every answer includes the guideline name and section.

The 2026 FHA floor loan limit for a one-unit property is $541,287, set at 65% of the conforming baseline. High-cost ceiling is $1,249,125.

My First Texas Home

ONE Mortgage

FL HFA Preferred

Every state. Every program. Current terms.

All 50 state Housing Finance Agencies: income limits, structure, and assistance amounts, updated as programs change.

Know who can do the deal before you call.

200+ lenders with DSCR, bank statement, foreign national, and agency overlays.

Who needs your call. Before you ask.

Per-deal cards with the exact reason and one action to take today. Stall detection flags files stuck 7+ days.

Martinez Rate lock expires in 3 days.

Patel Stale 28 days. Check in before the 30-day flag.

Chen In underwriting. On track.

Actively maintained. Not autonomously drifting.

Every query sharpens the knowledge base. Gaps get flagged, researched, and verified by a human before they ship.

4,847

queries processed

From scenario to answer

without touching a handbook.

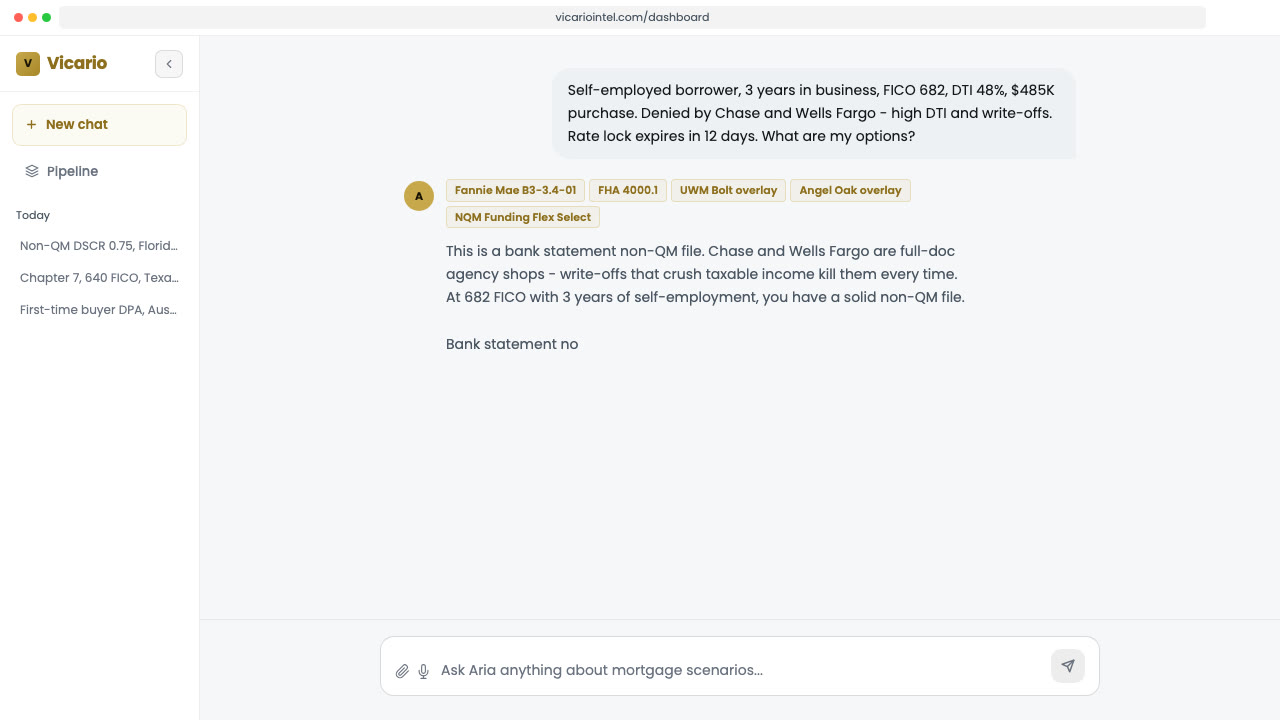

Describe the scenario.

Type any borrower situation in plain language. Self-employed, DSCR, employment gap, non-warrantable condo. Aria reads the context.

Aria reasons through it.

Aria cross-references agency guidelines, 50-state DPA eligibility, and lender overlays specific to your state and scenario type.

You get a research answer.

A specific program, a specific lender to call, and exactly what to verify before you send the file. You make the call.

Simple pricing. No per-query fees.

One flat monthly rate for individuals. Custom arrangements for teams and platforms.

Individual

For licensed MLOs who handle complex scenarios daily.

- Unlimited Aria queries

- All 50-state DPA programs

- 200+ lender overlays and pipeline analysis

- Lender routing by deal type

- Agency guideline intelligence (Fannie, Freddie, FHA, VA, USDA)

- Confidence-calibrated responses

Enterprise

Per organization, billed annually.

- Everything in the individual plan

- Dedicated onboarding

- White-label ready

We will reach out within one business day.